Why Contribute?

Key Takeaway

Experts generally agree that most people will need between 70 – 85% of their current income in retirement. Social Security will only provide a portion of that amount. You’ll need to have other savings and investments to have a successful retirement. Fortunately, your employer offers you the opportunity to save money for retirement with a tax-deferred retirement plan. Find out why investing in the employer-sponsored plan is one of the easiest and smartest things you can do to ensure you are financially prepared for your future.

HOW DOES MY PLAN WORK?

You elect to defer a percentage of your pay on a pre-tax basis. The amount is taken out of each paycheck and placed in the plan on your behalf. While in the plan, your money grows on a tax- deferred basis until you receive distributions.

WHY SHOULD I CONTRIBUTE?

Building retirement savings is the main reason to make your own contributions to the plan. An employer-sponsored plan is an easy and convenient way to save regularly for retirement. Plus, contributing on a tax-deferred basis allows your investments to grow at a much faster rate than a taxable savings program.

TAX-DEFERRED SAVINGS

Tax-deferred savings provide you with two important benefits: First, no federal income tax is deducted from the amount you defer into the plan. Second, the funds in your account keep growing without any federal taxes on the investment earnings. You don’t pay taxes until you begin withdrawing money.

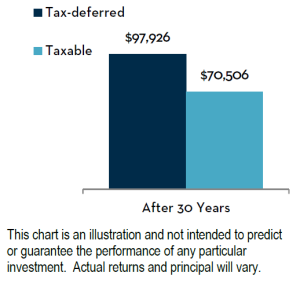

IS TAX DEFERRAL REALLY SUCH A BIG DEAL?

Yes! Take a look at the chart:

■ $1,200 in annual tax-deferred contributions.

■ 28% tax bracket.

■ $864 in annual taxable contributions ($1,200 after taxes).

■ 6% return on investments.

INVESTMENTS

Your plan offers you several choices for investing your contributions. You can select the investments that you are comfortable with and that you think will help you reach your investment objectives.

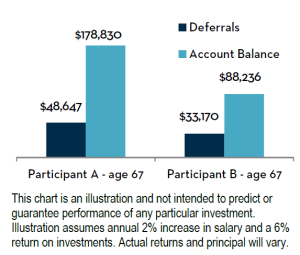

I’M YOUNG. CAN’T I WAIT A FEW YEARS?

For some people, retirement may seem a lifetime away, but don’t be tempted to put off saving. Each year it becomes more difficult to make up for lost time. Start as soon as possible. Consider the following example:

Participant A makes $25,000 and starts contributing 3% of salary at age 25. The account would be worth $178,830 at retirement.

Participant B has the same starting salary and also contributes 3% but doesn’t start contributing to the plan until age 35. Participant B’s account would be worth $88,236.

Participant A only contributed an additional $15,477 yet has an estimated final balance of $90,594 more than Participant B. Starting at age 25 provided Participant A with 10 more years of employee contributions, as well as 10 extra years for those contributions and their earnings to grow. No matter what your age, starting now will give you the best chance of securing a comfortable future.